{kind=link}

Happy Monday, Freebs! Earlier this summer, I received an email from Mindy, a fellow reader who wanted to share an amazing #FreebsSuccessStory with all of us… hers! It's an incredible story of hard work, dedication, and using frugality in your favor! Did I mention they paid off $400,000 of debts in 3 years? Yeah, this story is inspirational!

PS, do you have a #FreebsSuccessStory you want to share?? Every Friday you can share #FreebsSuccess, big or small, on Instagram and Facebook. It’s incredible what big – and small – results can come from simple changes. Check out last week’s FB and IG success stories, then come back Friday to share some of your own!

Without further ado, meet Mindy, her darling family, and hear about how SHE has earned financial success, and feels the relief of paying off $400,000 in debt, and now lives a debt free life!

Take it away, Mindy!

I’m Mindy, and I live in South Jordan, UT. I’ve been married to the man of my dreams for 22 years, and we have six kids. My husband, David, is a computer programmer and I am a stay-at-home mom. I have been homeschooling my kids for the past 3 ½ years, and have really been loving it! I enjoy reading, baking, interior design, scrapbooking, remodeling/building homes, traveling, and girls’ nights out.

I have always been conservative with money; more of a saver than a spender, and grew up in a home where money was managed carefully. My dad is a financial planner, and my mom has always been thrifty and resourceful in managing the household resources, so my siblings and I were taught well to put aside money for a rainy day, and plan for retirement while young. My husband’s family worked hard and didn’t spend frivolously, but didn’t have the same viewpoint on saving for the long term that mine did. He came into our marriage thinking that saving was a waste, because you couldn’t use the perfectly good money that you had just sitting there in the bank.

A couple of years into our marriage, when my husband had his own company building cabinets, one of our main clients closed up shop and left town, leaving behind many unpaid bills, including owing us about $13,000. We were devastated, because we had been counting on that money to be able to pay the mortgage, buy groceries, and pay suppliers, whom we owed for the materials. We started to live on credit cards in order to be able to put food on the table. His brother helped him get a job at a company where he learned to be a computer programmer, and we began to have a steady income. My parents lent us the money to pay back the suppliers, and my husband’s parents helped us figure out a fold down plan to pay off the credit cards. It took us a year or two, but we finally paid back my parents and all the credit cards. We learned many lessons from this, and never abused credit cards again, but we definitely still subscribed to some of society’s thinking in having car payments, school loans, home loans, second mortgages, and business loans. We thought (as most people do), that loans were normal and a necessity in life if you want to get ahead. The years went by, our income went up, we had more kids, and we took on more debt. We still were rather careful, and would try to pay off our cars early, but for the most part, didn’t think anything of having debt.

We built or remodeled every house we owned, and ended up making out pretty well on our homes each time because of the equity that we built, as we increased the value of the houses. In 2009, we saw an opportunity to get a good deal on land, since prices had plummeted with the recession, so we built our 5300 sq. ft. dream home in a nice, affluent neighborhood, but we did it for way less than most people would think. Because my husband grew up with a construction background, we did the general contracting ourselves, and as much of the labor as we (kids included) possibly could (cabinets, paint, trim, floors, etc.). We “squeezed every nickel into a quarter” by taking the extra time to find the best prices on everything. The garden tub for our master bedroom and the drinking fountain for our mudroom were both bought secondhand on KSL (online classifieds) for very cheap. They were practically new, and we just cleaned them up a little. We found fixtures and sinks in the clearance section at Lowe's, bought carpet at wholesale, and haggled on everything we possibly could.

Shortly after we moved in, my husband decided that he really wanted to open a restaurant. I was very reluctant, because by this time, I had read Dave Ramsey’s Total Money Makeover, and had seen the error of our ways in regards to debt. But he was very persistent, and I didn’t want to be a dream crusher, so I went along with it. We ended up borrowing about $100,00 on a home equity line of credit, and $45,000 from some investors, and the rest we cash-flowed through selling his nice car, and using some savings. My husband kept his programming job and we hired a friend to help us general manage the restaurant, but it still took up every remaining bit of time, money, and brainpower we had to keep it all running. Finally, after a year and a half of being open, we decided to close our restaurant and cut our losses. It was a devastating loss, emotionally and financially.

The “final straw” –

It was at this time, while we were still reeling from the loss and licking our wounds that I came back to the idea of setting a goal to become debt free once and for all. Because of our different backgrounds in how we grew up, we didn’t always see eye to eye in how our money should be managed. But since we were at rock bottom and so humbled, I knew it might be the right time to try to change things. My husband had an hour commute to work every day, and had asked me to get him some audio books from the library, so I got him Dave Ramsey’s Total Money Makeover. He actually wasn’t very thrilled about that, and told me that he was hoping for something more exciting, like an action novel. I told him to get started on that book in the meantime, and that I would go back to the library and get something else.

It worked out just as I had hoped, however. Once he started listening to the book, he began to have some hope that we could actually pull ourselves out of this hole, and we started more and more to be on the same page. A few weeks later, we were driving back from a family reunion trip, and since we had such a long drive in the car, we began to plan and dream. We dared to hope that perhaps we could pay off everything in 5 years, because as we ran the numbers, we started to see lots of possibilities. I still thought 5 years was a little ambitious at that point, but I figured we would shoot for the stars, and we would still be better off, even if it took us longer. We were making about $138,000 per year at the time, but our income quickly went up to about $162,000 during the course of this time period.

At this point, we figured out that we owed $418, 405.21, which was broken down like this: $282,500 on our mortgage, $93,765.10 on our home equity line of credit, $12,140.11 on our car, and $30,000 on a business loan from our investors.

Time for a change –

The day we were driving home and made this goal was January 1, 2012 and we knew we had to really change some things. In February, we filed our taxes, and since we had taken such losses, we got back every single penny we had paid in taxes for the previous year, which ended up being right around $55,000. (I know, crazy, right?) We took every bit of that and put it towards debt, paying off the investors and the car in full, and then taking the balance and putting it towards the HELOC (home equity line of credit). That really started the ball off rolling, and we had some good momentum. It was around this time, when I was looking for all the ideas I could to be more frugal, that I found Jordan’s blog. I immediately began implementing many of her ideas. One thing that worked really well for us was to open a separate checking account (I got paid $100 just for opening it), and use it as a place to set aside money in order to put it toward debt. We decided that we could spare $1000 from each paycheck so we had it automatically taken out of our check and put in there. Then when my husband would get his quarterly bonus (usually about $8000), we would also put it in there. As soon as we would get a big chunk, (like around $10,000) we had it set up in Bill Pay to electronically make a payment towards our HELOC. We also sold restaurant equipment and supplies that we had sitting in our garage and put that towards the debt. We rented out our basement to a friend and his four kids, and we agreed that he would buy all the household groceries and pay an extra $500 a month that went right towards our debt reduction. It also freed up the money that we would have spent on groceries to put to debt also. It was a win-win for both parties, and saved us both money.

Another big thing we did was have our kids step it up in paying for their own things. We required our teenage kids to pay for all of their own clothes, sports, entertainment, car insurance, etc. At first, they resisted and told us it wasn’t fair, and that none of their friends’ parents made them pay for their own stuff. But, we would just smile and tell them how lucky they were to be learning how to stand on their own two feet so early, and that their poor friends weren’t going to get to have that wonderful feeling of being able to say that they did it themselves! 😉 They would roll their eyes at us. Our son and daughter both got jobs at McDonald’s and worked 20-25 hours a week, along with their schoolwork and sports, and managed to do very well. Because our son’s goal was to serve a 2 year mission for our church and pay for it all himself, he ended up having to save 80% of each paycheck toward it, in order to earn it in time. Then he paid 10% tithing and lived on the remaining 10% for entertainment. He saved up the entire $10,000 needed in a year and a half, and he was so proud to say that he did it himself! Our daughter saved up $2000, and bought herself a car, and then, after switching from McDonald’s to Hobby Lobby and getting a better wage, proceeded to save another $6000-8000 towards college tuition and living expenses before she graduated high school. Our 15 year old son has a job as an after school janitor at an elementary school, as well as helping with some construction, and has saved up about $4000 already towards his mission and college as well. And by the way, the good news is that each of our older children at one time or another, have come to us later, and THANKED us for allowing them to have that good feeling of paying their own way!!! (Although my daughter told me never to quote her on that, so SHHH!!!! Don’t tell her!) 😉

When I see toys on clearance for a really good deal, I buy several and stockpile them, so that when my kids are invited to a birthday party (which is often, with lots of kids!), they just get to pick one out of our gift closet that they would like to give. Not only does it save me a separate trip to the store after an invite, it simplifies their choice, so we don’t have to wander through a whole store while they’re deciding what their friend would like. Also, I shoot to spend $5 or less on each gift (usually more like $3), but it always looks like a $10-15 gift, because I got them so cheap!

I am a mystery shopper, so I never pay for an oil change or safety/emissions inspection. I also can go out to eat, get hotel stays, groceries, and plants for my garden for FREE. That has been really fun and saved a lot! I also found out about unadvertised programs at my husband’s work that subsidized gym memberships and swimming lessons. They also had a “pay for good grades” program that gave FREE money to save for college. I found a program where I get all my homeschooling supplies and curriculum for FREE, so we weren’t paying any school fees, but I get to give my kids a superior and customized education at home. They have even taken concurrent enrollment college classes and earned college credit for free.We got rid of cable and got a digital antenna that paid for itself in a couple of months, so now we don’t pay anything.

Small changes lead to big results!

It didn’t take long before all these changes started adding up and giving us lots of momentum in our journey to being debt-free! The kids stopped asking us to pay for things, the balance of debt started going down, and best of all, we didn’t feel like we were deprived! We had figured out that it can be FUN to try to beat the system! After that first year, when the anniversary of the closing of our restaurant was approaching, we saw that we were so close to having all the business debt paid off, so we really put it in high gear, my husband put in extra hours on the side doing computer consulting, and we managed to pay that part off by the year mark.

As we entered the second year, we didn’t think we could do that much again. We were down to just our mortgage, so it was still almost $300,000. David started running numbers and decided that if we could pay off $100,000 each year, we could have it all gone in less than 3 years, which would be a year less than our original goal of 5 years total. He figured that if we could come up with an extra $8333 each month to put towards debt, that it was doable. I wasn’t sure about it, because the first year, we had some big momentum with the tax return and the sale of our restaurant equipment. But we still weren’t paying for groceries ($1000 per month savings) and we had that extra $500 from our renter (about $1500 per month total we could use, or $18,000 per year). plus we still had the $2000 still coming out of the paycheck automatically ($24,000 per year). He knew that we had 4 quarterly bonuses of $8000 or so each ($32,000), so that all added up to $74,000 right there. It started to feel more and more doable, so we set our goal of paying off $100,000 per year. We reached that goal, and then did it again the next year as well. By then, we no longer had the renters, but our income and bonuses had gone up quite a bit,

…and we were already in the mindset of living off of a quarter or a third of what our salary was.

Even though there were many hard things and sacrifices we made, the great feeling of seeing that balance go down became the payoff that we needed to help us keep going. My husband was especially driven, and he would check the balance every day. He’s very goal oriented, so when he decides to do something, he’s all in!

We still had weekly date nights, but we would always use a coupon or share a meal when we went out to eat, or we would go do something else that was cheap or free. We kept our vacations very simple, even holding off and simplifying our family tradition of taking each of our kids on their own trip when they turn 10. We had one child turn 10 during that time, and we found an extremely cheap cruise to Hawaii instead of the more elaborate international trip we usually opt for. (He loved it, and didn’t feel slighted at all!)

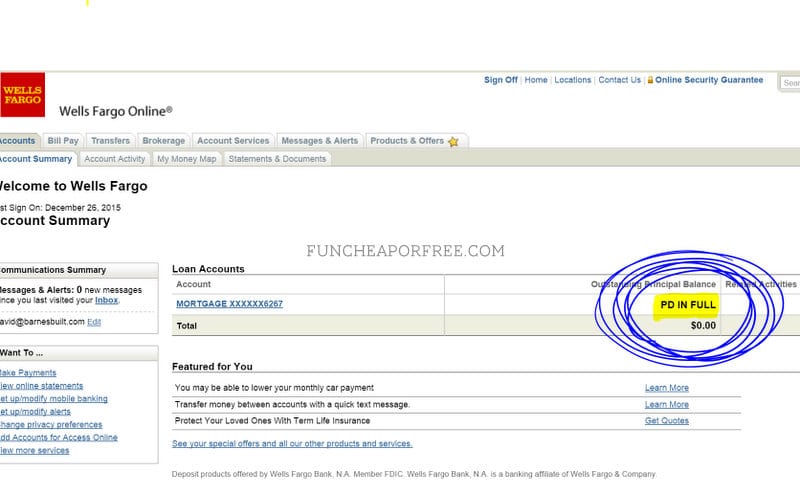

We ended up finally making the final payment on our mortgage on November 27, 2015, which was Black Friday. It was meaningful to us because it was a day when most people were out spending money, a lot of them putting it on credit, and yet we were doing the opposite! It was so surreal, and such an amazing feeling to log in and see that “Paid in Full” on our account! It ended up taking us 3 years and 11 months from beginning to end! We still look at each other sometimes, and say, “We’re debt free!” Our home, which we built for $375,000 and originally put down $100,000 on, is now paid off and worth somewhere between $550,000 – 600,000.

To celebrate, we booked a slot on the Dave Ramsey show in January and we drove to Tennessee where his studio is located. It was such a great feeling! Here is a video clip of that appearance: https://www.youtube.com/watch?v=IpMc-aksHro

What was/is the hardest part? What roadblocks, challenges, or setbacks did you/do you encounter?

I would say one of the hardest things in this whole process has been the feeling of being alone and nobody really understanding what we were trying to do. Society tells us that it’s totally normal to have debt, and we have all bought into that (us included, at one point), and so it seems so impossible to be out of debt. People we told about our goal would look at us a little funny, or tell us why that wouldn’t be possible for them to do. As Dave Ramsey would say, we were “weird”. So, at a certain point, we became more and more reluctant to tell people about it. We knew only a few couples that had their home paid off and they were our inspirations. But, we have come to realize in these last few months, that even though we don’t want to seem like we are boasting and we aren’t usually too apt to tell people about it, the world needs to hear more people come forward, and show that it’s POSSIBLE.

The best part of it all is the HUGE RELIEF we have, and the weight it has taken from our shoulders! Also, we have the feeling that if we accomplished this, what else could we do that seems impossible? Also, I have seen such a difference in our kids from how they were before. They don’t take things for granted, they don’t ask for things to be paid for, they just are responsible for themselves. Our two oldest are totally self-sufficient and support themselves completely. And when we do send them a box of groceries from Amazon out of the blue, they are SO grateful, because they weren’t expecting it! That has been an amazing side benefit of this whole thing! It was so worth it to endure all the complaining and eye-rolling! 😉

It's been an incredible journey!

I would encourage everyone to set a goal financially that you would like to accomplish.

It doesn’t have to be on such a grand scale as paying off your house to start out with. But as you work hard and get closer to accomplishing it, there is a thrill that comes and momentum to help you keep at it, even when it’s hard and nobody understands. Then, when you have achieved that, dream a little bigger, and set a goal that might seem impossible. Use that momentum you gained to keep it going!

Also, challenge every expenditure! Do you really need it? Is there some way to get it cheaper, or even free? Could your kids take on their own expenses? Do you have things to sell off that you don’t need or use anymore? There is ALWAYS a way to still have a rich, full life and be frugal at the same time!

I want to thank Jordan for inviting me to share our story, and for giving me the platform to do so. She has been an inspiration to me in many ways – helping me rethink ways to have everything I need and want, and to enjoy being frugal. I believe, as she does, that being frugal doesn’t have to be drudgery and deprivation! It can be fun, and I can have nice things for a fraction of the price that one might think that it would cost. Her great attitude and tips have been an inspiration to me!

* * * *

I am beyond inspired! Mindy and her family buckled down, with a goal in mind, and it paid off! Literally, paid off! Thanks so much for sharing your story with us, Mindy!

Do YOU have a #FreebsSuccessStory you’d like to share?? We’d LOVE to hear it!

Email me, jordan@funcheaporfree.com if you want to share your story on the blog! Otherwise remember that every Friday you can share #FreebsSuccess, big or small, on Instagram and Facebook. It’s incredible what big – and small – results can come from simple changes. Check out last week’s FB and IG success stories, then come back Friday to share some of your own!

Want to make some huge changes in your own life?

If you want to start from the beginning, and get all my tips for managing your day-to-day finances with my Budget Boot Camp program! It has all my secret sauce in once place, and HOURS of things that have never been talked about on this blog!

It’ll hold your hand and walk you through everything, every step of the way. Head to BudgetBootCamp.com for more info! (PS use the code FCFBLOG to get an extra 10% off!)

I am touched and inspired by you all every day and hope you know this is exactly why I do, what I do, without taking a paycheck. We are changing families, and the world if I may be so bold, and it’s pretty darn exciting. I LOVE MY FREEBS!

Give me a break. You were making $200k a year. You could have been doing great without all the “scrimping” if you didn’t get yourself in so much debt in the first place. Poor choices and hardly a great success. Try getting yourself out of 100k in debt when you make 35k a year. That’ll be something worth acting happy about.

Thanks for sharing your story. Truly inspirational. We are also working on our mortgage, luckily I have always been allergic to debt, so I was spared the hard lessen you went through, but it will be an incredible feeling to have the ‘Full paid’ stamp on our mortgage, I really can relate to your feelings. Keep up the good work 🙂

Great story! Thank you for sharing! There is nothing better than helping your children enjoy the benefits of working hard for honest work. I feel like I grew up always having a job, but those middle school & high school activities seem to crowd out their time to work. This past year, we have had our two oldest start paying for various things too, and get a job. They have LOVED working and are managing their time and their money so much better, and I am not paying for a lot of extras like I used to.

What an amazing success story! 🙂